What to Do With 5 Million Dollars

However, accumulating $5,000,000 isn't exactly easy. You'd probably need to be in the top 1% to reach $5M in net worth. That's about $420,000 per year in household income. Here are some of the top income earners:

- Executives of large companies and public institutions. Eric Barron, the president of Penn State University, made over $800,000 last year.

- Highly paid professionals such as surgeons, lawyers, and investment bankers. A highly experienced anesthesiologist can make $500,000 per year.

- Business owners.

- Entertainers, sports stars, and other celebrities. Floyd Mayweather topped the list in 2018 with $285 million of income. George Clooney came in second with $239 million. Most of that is from the sale of his tequila company, not bad at all.

These people tend to be very successful and $5 million isn't out of reach for them. I did a little internet research and it seems people who reached "pentamillionaire" status aren't quite as ready for retirement as you'd think. By the way, nearly three million households are worth over $5 million in the United State. That's a lot of rich folks.

Take my poll at the end of this post. 40% of voters don't think $5 million enough to retire on. That's over 5,000 people which is much more than I expected. Wow, please leave a comment and let us know you need more.

*Updated for 2019.

A Spending Problem

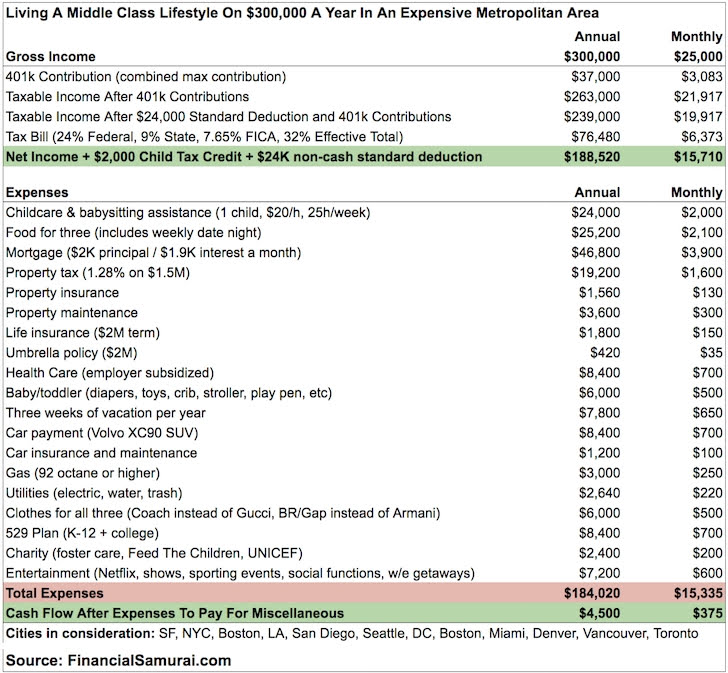

One issue with earning the top 1% is that you spend like you're rich. Which you are, but it probably isn't sustainable. You can't make that much income forever. Last time, I used a profile of a Canadian couple who was having a rough time after the main breadwinner was laid off from his $300,000/year job. This time, I'll use an example from Financial Samurai. Sam published a post about how much it costs to live in an expensive city – Why households need to earn $300,000 a year to live a middle-class lifestyle today. Here is the expense spreadsheet.

This family barely has anything left after tax, deduction, and expenses. The only significant savings they have is their retirement and home equity. They are maxing out their 401k contributions every month. Nice job on that front. However, this family will be in huge trouble if one of them loses their job. It is unbelievable how close to the edge this family is living. Unfortunately, $300,000 doesn't go very far in San Francisco, New York, and other expensive cities. At this level of expense, this family will need at least $5 million to retire. I don't see how they'll get there with this saving rate.

Personally, I think this family can reduce their monthly expenses tremendously. If they set their sights on FIRE (financial independence retire early), then I'm sure they can get rid of the Volvo XC90 and drive a cheaper car. Their food expense also seems very high to me. Lastly, they are spending a lot of money on their kids. Kids aren't that expensive if you're a little frugal. There is a lot of room to cut back on this budget. However, regular people are living for today and they aren't thinking about financial independence. That's why I'm trying to spread the word about FIRE through Retire by 40.

Regular Folks

Okay, that's enough about rich people and their first world problems. If these wealthy households can't figure out how to live like normal people, then they will have to deal with the consequences. For the rest of us, we need much less than 5 million dollars to retire. Here is how to calculate your ballpark target for early retirement.

- Track your expenses

- Take your annual expense and multiply it by 25

- Add some margin if you have expected expenses such as college expense or long-term care.

RB40 household example

- Our annual expense is about $55,000.

- $55,000 multiplied by 25 = $1,375,000

- Margin: $125,000 for college

So we'd need about $1,500,000 of investable assets to have a good chance of a successful retirement. You probably shouldn't include your primary residence in this calculation.

Currently, we have over $2 million invested so I'm pretty comfortable with my early retirement. However, this isn't quite enough security for Mrs. RB40. She needs a bit more margin and that's one of the reasons why she isn't quite ready to retire yet. (Besides, she likes her job). Here is my opinion on our early retirement based on the current expense.

- $1.5 million – Barely enough to FIRE. We'll probably be okay, but we need to have some backup plans. I'll continue to blog and hustle to make some income. At this level, Mrs. RB40 won't feel financially secure.

- $3 million – Comfortably FIRE. This gives us some margin for errors. I wouldn't have to worry much about generating active income. Mrs. RB40 will feel financially secure enough to pull the cord and retire early. We could withdraw 3% and that's pretty much foolproof. As long as our spending stays at this level, we'll be fine. You can see the analysis below.

- $5 million – We're rich! $5 million is more than enough. If we can keep our lifestyle inflation reasonable, we will have a good base to build wealth for future generations or donate it to a good cause.

RB40 household with $3 million

I logged on to my Personal Capital account and used the Retirement Planner to see how we'd do with $3 million in savings and spend $90,000 per year. There is a new feature where you can see how you'd do with different savings and income. It's pretty neat. I created a new scenario with these parameters.

Income

- Savings: $3,000,000

- Social Security: $25,000/year at 67

- Social Security (Spouse): $25,000/year at 67

- Blogging: $30,000 per year for 10 years. I made $65,388 from blogging last year, but the blog income is unstable. I'm pretty sure this income will crater as soon as we see a recession.

Spending Goals

- Retirement Spending: $90,000 per year starting this year.

- College: $40,000 per year from 2029 to 2032.

Here is the result – You're in very good shape for retirement. We forecast a 95% chance your portfolio will support your goals, including $90,000 per year in basic retirement spending.

I also ran this scenario through FireCalc and other retirement calculators. They all agree that $3 million is plenty for us. Withdrawing 3% is very conservative and the portfolio should last indefinitely.

Sign up with Personal Capital if you don't have an account yet. The Retirement Planner is a fantastic tool that use your real data to help you plan for retirement. I highly recommend it for DIY investors.

Can you retire with 5 million dollars?

Lastly, the problem with money is that you always think you need more. I figured we'd feel wealthy if we ever reached $5 million in net worth, but maybe that's just because we're not there yet. It's easy to say $5 million is plenty to retire on. However, I might change my mind once we get there. I'll update this post when we reach $5 million and let you know what we think then. It will probably take me a decade to get there, though.

It seems people who have $5 million also think more is better. I read some discussions in various forums and people hesitate to retire even when their expenses are under control. It's tough to find "enough." That's the one more year syndrome. Or is it one more million bucks syndrome? You can't buy time. You have to take that into account when it comes to retirement. Don't wait too long if you can retire comfortably. You need to enjoy life while you're young and healthy.

![]() Loading ...

Loading ...

Do you think you can retire with 5 million dollars?

*Sign up with Personal Capital if you don't have an account yet. The Retirement Planner is a fantastic tool that use your real data to help you plan for retirement. I highly recommend it for DIY investors.

The following two tabs change content below.

- Bio

- Latest Posts

Joe started Retire by 40 in 2010 to figure out how to retire early. After 16 years of investing and saving, he achieved financial independence and retired at 38.

Passive income is the key to early retirement. This year, Joe is investing in commercial real estate with CrowdStreet. They have many projects across the USA so check them out!

Joe also highly recommends Personal Capital for DIY investors. They have many useful tools that will help you reach financial independence.

Get update via email:

Sign up to receive new articles via email

We hate spam just as much as you

What to Do With 5 Million Dollars

Source: https://retireby40.org/can-retire-5-million-dollars/

0 Response to "What to Do With 5 Million Dollars"

Post a Comment